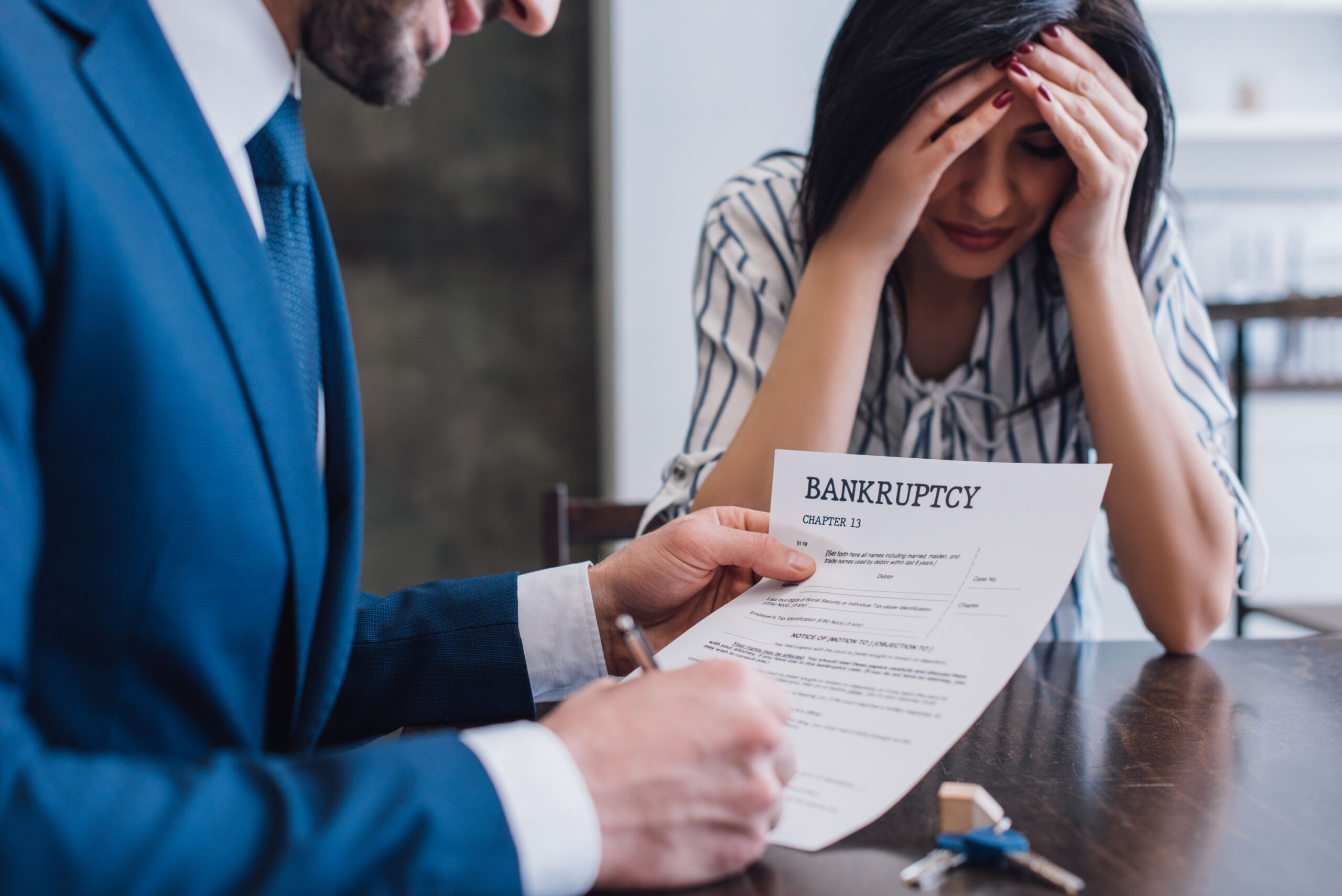

If you have decided that bankruptcy is the right choice for you, you may be worried about your family home. Even if you can’t afford the payments on your other debt, you may be able to keep your home. How is that possible? Clients can participate in the New Jersey Bankruptcy Court’s Loss Mitigation Program as a way to save their home. This is a program to restructure your mortgage payments.

File Within 30 Days

The timeline for loss mitigation is fairly strict. In New Jersey Bankruptcy Court, you must apply to the loss mitigation program within 30 days of your initial bankruptcy petition. Failure to meet this initial deadline will require to file a motion. This obviously becomes more time consuming and expensive. Once your application (or motion) is granted, there is some flexibility on both sides. This gives both parties plenty of time to come to an agreement and a workable solution.

Loss Mitigation Sessions and Considering Different Solutions

Early in the process, you and your creditor can begin working toward an agreement. To facilitate this process, the New Jersey Bankruptcy Court usually requires the parties to utilize the “DMM Portal” system. The lender will submit the packet to the debtor’s counsel through the secured portal and in response, you and your legal team at Lucid Law will submit all of the responsive documents to the lender through the portal. The DMM Portal is a secure online system and it ensures that all document exchanges and communications between the debtor and the lender are tracked. In this way, New Jersey’s Bankruptcy Court has given both sides of the loan modification process the peace of mind that the process is fair and that documents are not lost and do not become stale – as too often happens when individuals try to obtain Loan Modifications outside of the Loss Mitigation Program.

Through a number of document exchanges and communications with your lender or servicer, your legal team at Lucid Law will discuss different solutions and figure out the requirements for each option with your lender. The options available to you depend largely on how much you owe, what you can afford, and your home equity. Some choices the lender will offer include loan refinancing, forbearance, short sale, and loan modification. If you choose to surrender the property or do a short sale, you will not be able to keep your home, so it’s important to be upfront with your creditor, and your legal team at Lucid Law, regarding your intentions.

File the Necessary Paperwork

Both refinancing a home and modifying a loan are significant and expensive processes, so you should be ready to complete a substantial amount of paperwork throughout the course of the program. As you proceed, you must provide status updates to the bankruptcy court and stick to the agreed-upon schedule. It’s likely that your creditor will also require a substantial amount of paperwork from you. Many companies now use an online portal that allows you to directly upload pay stubs, home appraisal documents, bank statements, and other documents. This minimizes the risk of lost paperwork and allows the company to process your documents more quickly.

Final Resolution or Settlement

There may be some negotiation between you and your loan provider. Make sure to keep the bankruptcy court updated on these proceedings. Once you come to an agreement regarding your mortgage, you must file the final settlement or agreement with the bankruptcy court. They have to approve it before it becomes finalized and goes into effect. If the two parties cannot reach an agreement, the home may become part of the bankruptcy process. This can cause the home to be subject to foreclosure.

Is the New Jersey Bankruptcy Court’s Loss Mitigation Program the right choice for your family? If so, call Lucid Law at 908-350-7505 to schedule a free consultation.