Prevent Financial Failure Through Filing for Bankruptcy

Financial challenges can arise unexpectedly in the bustling town of Bridgewater, NJ, leaving individuals and businesses grappling with overwhelming debt. When the storm of financial uncertainty hits, having a reliable Bridgewater bankruptcy attorney by your side becomes crucial.

Short Summary:

- Bankruptcy is a strategic financial move, not a failure, and there are three main types: Chapter 7 for liquidation, Chapter 13 for repayment plans, and Chapter 11 for businesses.

- Bankruptcy can shield against creditor actions and is a strategic option for challenges like harassment, foreclosure, and sudden financial strains.

- Understand eligibility criteria for Chapters 7, 11, and 13 to ensure a clear overview of income, expenses, and debt limits.

- A concise step-by-step guide to filing for bankruptcy is listed below, from assessment to discharge or reorganization.

- The means test is crucial for Chapter 7 eligibility, comparing income to the state median.

- Debt consolidation is a strategy to simplify payments and potentially lower interest rates.

- Recognize creditor harassment and preventive measures, including knowledge of rights and open communication.

- Protect your home from foreclosure, including negotiation, refinancing, and Chapter 13 bankruptcy.

- A Bridgewater bankruptcy attorney offers personalized attention, tailoring strategies for a stable financial future.

At Karina Lucid Law, we understand the complexities of bankruptcy law and are dedicated to guiding you through the process with proficiency and compassion.

What is Bankruptcy?

At its core, bankruptcy is a legal process designed to offer individuals and businesses a fresh financial start when overwhelmed by debts they cannot repay. It’s not a sign of failure but a strategic move to regain control and rebuild. There are different types of bankruptcy, each serving unique purposes.

What are the Main Types of Bankruptcy?

Bankruptcy is not a one-size-fits-all solution. Rather, it comes in different chapters, each tailored to specific circumstances. Here’s a breakdown of the main types of bankruptcy in the United States:

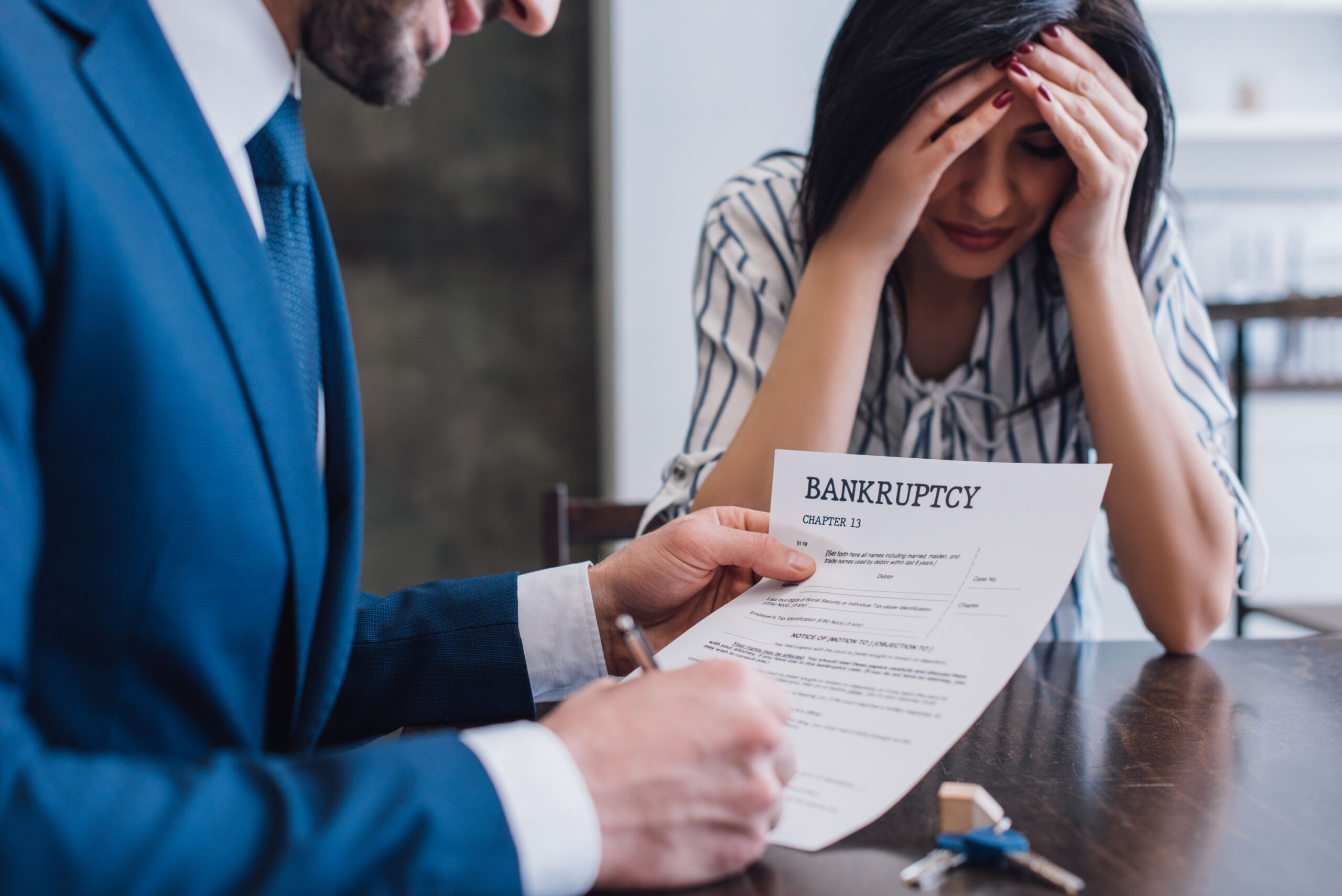

- Chapter 7: Commonly known as liquidation bankruptcy, Chapter 7 involves selling non-exempt assets to pay off creditors. It’s often suitable for individuals with limited income and significant unsecured debts. The process is relatively quick, providing a fresh start by discharging qualifying debts.

- Chapter 13: Chapter 13 bankruptcy is a reorganization plan for individuals with a regular income. Rather than liquidating assets, it involves creating a manageable repayment plan over three to five years. This chapter benefits those who want to keep their assets, like a home, and catch up on missed payments.

- Chapter 11: Chapter 11 bankruptcy is primarily designed for businesses but can also be utilized by individuals with substantial debts. It allows for the reorganization of debts while the business continues its operations. This chapter is more complex and expensive, often chosen by large corporations or individuals with substantial assets.

When Should I Consider Bankruptcy?

Filing for bankruptcy can offer a lifeline when facing overwhelming debt, providing a legal pathway to financial recovery. Bankruptcy acts as a shield, legally protecting you from aggressive creditor actions and offering a structured idea to address and resolve financial difficulties.

If persistent creditor harassment, looming foreclosure, or repossession threats are causing distress, bankruptcy’s automatic stay can halt these actions, offering a moment to regroup.

Sudden job loss, medical expenses, or divorce-related financial strains may also make bankruptcy a strategic choice, allowing for the restructuring or elimination of certain debts. While not a decision to be taken lightly, consulting with a skilled Bridgewater bankruptcy attorney can clarify the matter.

How Do I Become Eligible for Bankruptcy?

To be eligible for bankruptcy, the specific chapter you’re considering will have distinct criteria. Here’s a brief overview of Chapters 7, 11, and 13:

- Chapter 7: Chapter 7 bankruptcy is available to individuals, businesses, and entities. Eligibility is determined through a means test, evaluating your income, expenses, and ability to repay debts.

If your income is below the state median or you pass the means test, you may qualify for Chapter 7. However, individuals with higher incomes may be required to file under Chapter 13.

- Chapter 11: Chapter 11 bankruptcy is primarily designed for businesses, although individuals with substantial assets may also use it.

There are no strict income limits for Chapter 11, making it a more flexible option. Entities, including corporations and partnerships, commonly use Chapter 11 to reorganize and continue operations while developing a repayment plan.

- Chapter 13: Chapter 13 bankruptcy is for individuals with a regular income. It involves creating a manageable repayment plan over three to five years. Eligibility is determined by the amount of secured and unsecured debt you have, with specific limits for each type.

What is the Process for Filing Bankruptcy?

Filing for bankruptcy consists of several meticulous steps:

- Assessment: Evaluate your financial situation and determine if bankruptcy is appropriate.

- Credit Counseling: Undergo credit counseling from an approved agency within 180 days before filing.

- Choose Chapter: Select the proper chapter (7, 11, or 13) based on your eligibility and financial goals.

- Complete Forms: Fill out the required bankruptcy forms, detailing your assets, liabilities, income, and expenses.

- File Petition: Submit your petition and forms to the bankruptcy court in your jurisdiction.

- Automatic Stay: An automatic stay is initiated upon filing, halting creditor actions.

- Trustee Appointment: A bankruptcy trustee is assigned to oversee your case.

- Creditors Meeting: Attend the meeting of creditors, where the trustee and creditors may ask questions.

- Repayment Plan (Chapter 13): If filing Chapter 13, propose a repayment plan to the court for approval.

- Financial Management Course: Complete a post-filing financial management course.

- Discharge (Chapter 7): Receive a discharge of qualifying debts in Chapter 7 or complete the approved repayment plan in Chapter 13.

- Reorganization (Chapter 11): For Chapter 11, work on reorganizing debts and restructuring the business.

What is the Means Test?

The means test is a financial evaluation determining eligibility for Chapter 7 bankruptcy. It compares your income to the state median; if below, you likely qualify. If above, further analysis considers disposable income and expenses. Passing allows Chapter 7 filing; failing may lead to Chapter 13.

What is Debt Consolidation?

Debt consolidation is a financial strategy combining multiple debts into a single, more manageable payment. That often involves obtaining a consolidation loan to pay off existing debts.

It simplifies repayments, potentially lowers interest rates, and offers a structured approach to clearing debts. However, success depends on securing favorable loan terms and addressing the underlying financial habits that led to debt accumulation.

What is Creditor Harassment?

Creditor harassment involves persistent and intrusive actions by creditors seeking debt repayment, such as excessive calls, threats, or intimidation.

To prevent it, know your rights under the Fair Debt Collection Practices Act (FDCPA), maintain open communication with creditors about your situation, and consider sending a cease and desist letter.

How Can I Stop the Foreclosure of My Home?

You can take steps to protect your home from foreclosure. Options include negotiating with your lender for a loan modification, refinancing, or pursuing a repayment plan. Filing for bankruptcy, specifically Chapter 13, can halt foreclosure and provide a structured plan to catch up on missed payments.

How Can a Bankruptcy Attorney Help Me?

At Karina Lucid Law, we understand that each client is unique, and so are their financial challenges. Our commitment to providing personalized attention sets us apart.

A Bridgewater bankruptcy attorney from our firm will take the time to understand your specific circumstances, tailoring strategies that address your immediate concerns while laying the foundation for a more stable financial future.

Work With Our Bankruptcy Attorney Today!

In the face of financial uncertainty, the support and guidance of our Bridgewater bankruptcy attorney can make all the difference. Karina Lucid Law is dedicated to empowering individuals and businesses in Bridgewater, NJ, to overcome financial challenges and embark on a path toward renewed financial health.

Call us and get a free consultation today! Aside from bankruptcy, we also offer legal services on estate planning.