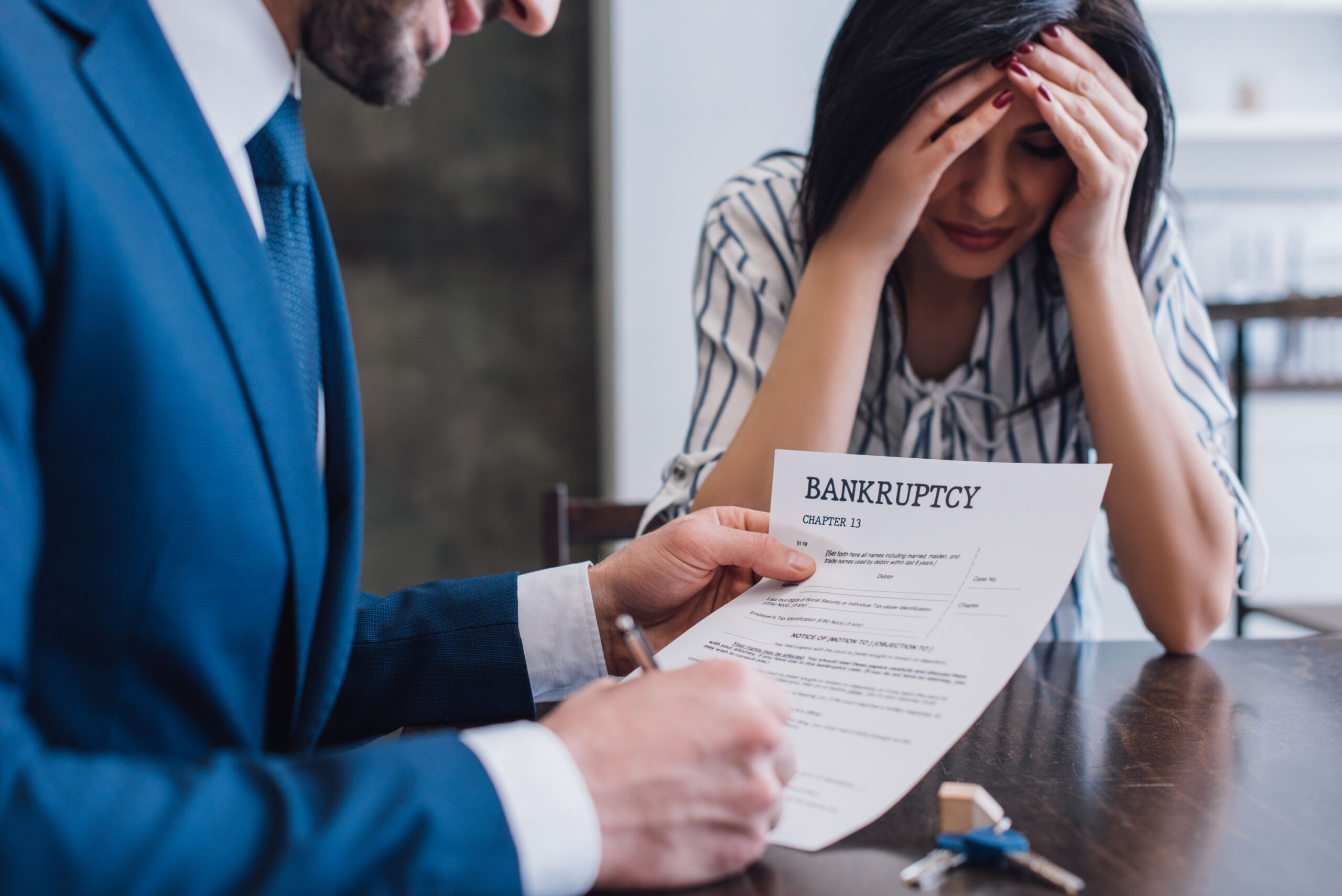

To qualify for a Chapter 7 bankruptcy in New Jersey, you must meet certain eligibility requirements regarding your current income. One of those requirements is the New Jersey means test. In other words, the test takes into account your financial means and income. Those who make too much money may not be able to file for Chapter 7 bankruptcy.

Remember that debtors who successfully use Chapter 7 are able to have most (if not all) of their debts discharged. Hence, they can then start over with a clean financial slate. Chapter 7, however, is not for those who have a high enough be able to start paying back their debts.

These debtors have the “means” to eventually get out of debt. Therefore, they will need to restructure through Chapter 13 rather than liquidation through Chapter 7.

The means test weeds out the higher income earners from taking advantage of Chapter 7. Thus, depriving their creditors of recouping at least some of their outstanding debt. Chapter 7 is attractive not only for the discharge of debts, but also because it takes less time to complete. Chapter 7 bankruptcy can be over in about one year, whereas Chapter 13 takes three to five years.

The first step in the means test

The first step is to compare the household income of the debtor with median income levels in their area. Specifically, the test looks at the income of the debtor for the six months prior to the bankruptcy filing date. That amount of income is then doubled and compared with the median income level of a household with the same number of earners in the family in that state. If the income of the debtor family—even when doubled—is still below the median income level for the family size in that state, then the debtor has passed the means test. The debtor may file for Chapter 7 bankruptcy.

For bankruptcy cases filed after May 1, 2018 in New Jersey, the median income level for one earner is $66,284. It increases to $81,054 for two people, $98,174 for three people, and $121,226 for four people. So, to meet the means test, your income—even when doubled—must still be below these figures.

If you do not meet the first step of the means test—that is, your income was higher than the median income of the same-sized family—this is not the end of the road. You may still be able to file for Chapter 7 bankruptcy by further qualification which takes a closer look at your income and expenses.

You are allowed to deduct living expenses based upon standard IRS allowances from your income. Once these expenses are deducted from the debtor’s income, if there is income remaining, the debtor must proceed with Chapter 13 bankruptcy. If nothing remains after living expenses are deducted, the debtor qualifies for Chapter 7 protection.

Contact Us

Navigating bankruptcy on your own can be difficult and downright dangerous. We can help you make the right choice with regard to bankruptcy. Let us help you back on your feet and moving forward again. Don’t lose hope, and let’s work together to jumpstart a new chapter in your life! Contact us today.